{kind=link}

Every business has a supply chain that is key to their success. However, inventory management is too often overlooked, until it’s too late. Find out in this article how to improve your inventory management and save time and money on your supply chain.

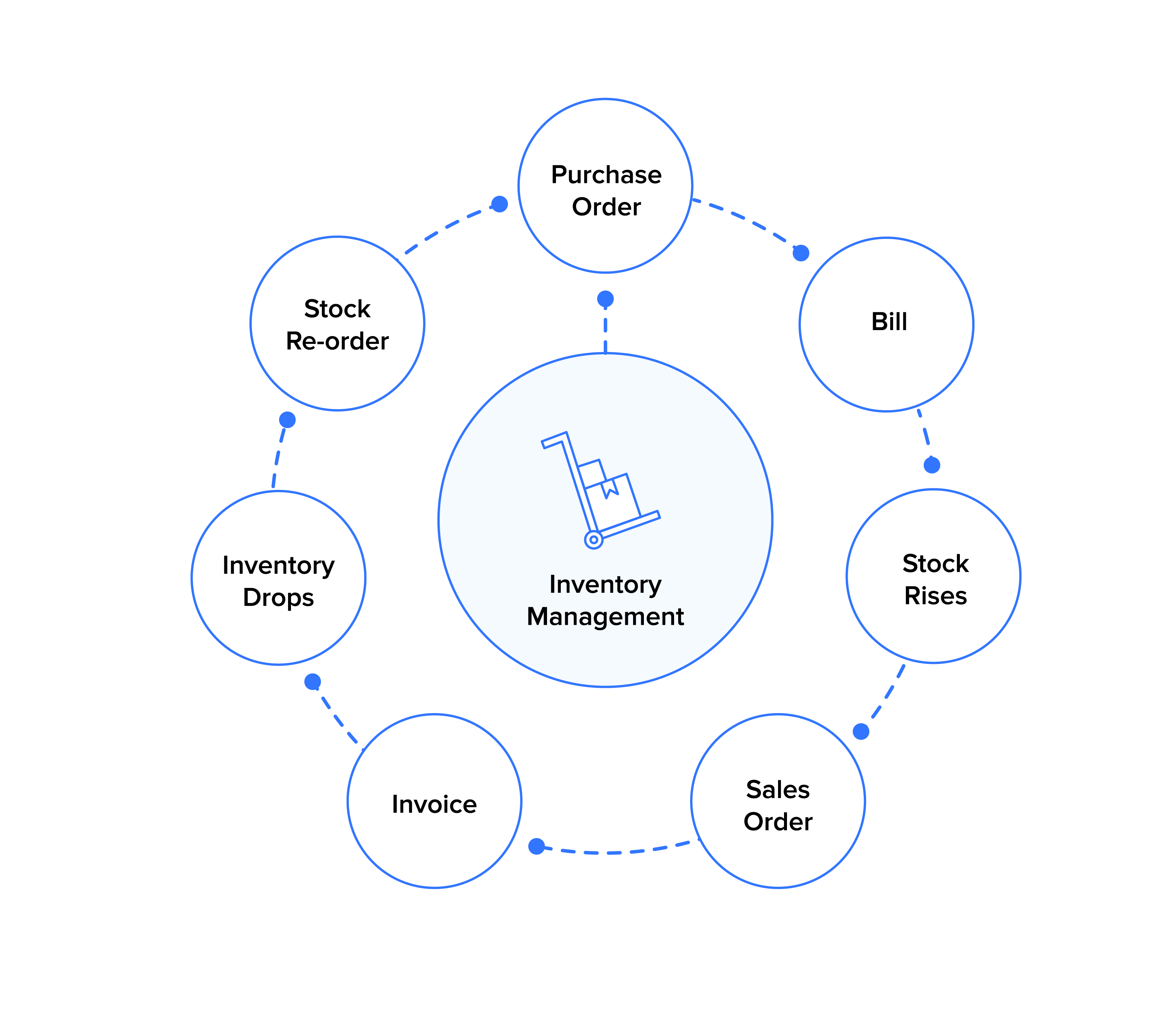

What is Inventory Management?

Inventory management is the process of tracking and managing the quantity, type, and location of assets in an organization. It is one of the most important aspects of a company’s supply chain, as it helps ensure that products are available when they are needed, and that costs are minimized.

One of the most common mistakes companies make when it comes to inventory management is over-ordering. This happens when a company orders too much of a particular product, and then can’t find enough to meet demand. Over ordering can lead to wastefulness, as products that could have been used instead are simply thrown away.

In order to avoid over ordering, companies must have accurate estimates for their needs. This information can be gathered through surveys or customer feedback, or through tracking sales data. Once an estimate has been made, companies must keep track of actual inventory levels in order to make sure that they’re not exceeding their limits.

If an organization’s inventory levels are consistently high, it may be time for them to reevaluate their supply chain strategy. Over ordering can also lead to lost profits due to higher costs associated with excess inventory. By using inventory management techniques, businesses can ensure that their supply chains are running smoothly and profitably.Categories

Health Condition

Mental Health

Fitness

Food & Diet

Wellness TopicsCategories

Health Condition

Mental Health

How to Implement Inventory Management?

Inventory management is the process of systematically tracking and managing the quantity and type of inventory that a company possesses. By doing so, businesses can ensure that they are always able to meet customer demand while minimizing the costs associated with excess or wasted inventory.

There are a number of different methods for implementing inventory management, and it is important to find the approach that works best for your business. Here are three tips for choosing an inventory management strategy:

1. Consider your business’s needs.

First, you need to consider your business’s specific needs. For example, some businesses need to maintain tight control over inventory in order to meet strict deadlines, while others may prefer a more relaxed approach that allows for more gradual stock changes. Ultimately, you need to find an approach that works well for your company and meets your specific needs.

2. Use stock analysis tools.

Second, use stock analysis tools to help you determine how much inventory your business actually needs. These tools can help you identify which items are selling well and which ones are in short supply. This information will help you determine how much inventory to keep on hand.

3. Make changes as needed.

Finally, keep an eye on sales trends and sales history in order to make changes as necessary. This approach enables you to adjust inventory levels as needs change. Inventory control is not the only way to minimize the cost of your supplies—other practices can help you cut costs either by increasing productivity or making purchases more wisely.

Basic Functions of Inventory Management

Inventory management is the process of monitoring and controlling the amount of resources that a business has available to produce products or services. Managing inventory requires understanding basic concepts such as capacity, demand, and supply.

Capacity is the maximum amount of a product or service that a business can produce in a given period of time. Demand is the maximum amount of a product or service that customers are willing to purchase in a given period of time. Supply is the amount of a product or service that businesses have available for sale.

Businesses must manage inventory to ensure that they have enough resources to meet demand while avoiding overproduction and shortages. Inventory management can be divided into two main categories: strategic and tactical. Strategic inventory management focuses on long-term planning and forecasting, while tactical inventory management focuses on meeting short-term demand.

There are five key principles of effective inventory app: control, allocation, disposition, accumulation, and accountability. Control means managing inventory so that it remains within predetermined limits set by the business. Allocation means deciding how much of each product to produce and how to distribute it among different factories and warehouses. Disposition means selling or using inventory according to business needs.

How to Manage Your Supply Chain?

Inventory management is one of the most important aspects of a successful supply chain. It’s critical to ensure that you have the right amount of inventory available at the right time so that you can meet your customer’s needs. Here are some tips for managing your inventory:

1. Keep track of your inventory levels. Keep track of what you have in stock, what you’re ordering, and what you’ve sold. This information will help you determine whether you need to order more products or reduce your inventory.

2. Plan for future needs. Make sure you have enough products in stock to meet any potential future needs. For example, if you expect to receive a new shipment of products in two weeks, make sure you have enough product to fill that order.

3. Order only what you need. Don’t order more products than you need to meet current and future customer demand. This will help keep your inventory down and free up space in your warehouse for new products.

4. Sell excess inventory. If an item doesn’t sell within a certain period of time, sell it as surplus inventory instead of keeping it on hand as stock. This will free up space in your warehouse and allow you to purchase more product to meet your customers’ demand.

Conclusion

Inventory management is a critical part of optimizing your supply chain. Not only does it help to keep your business running smoothly. But it can also prevent costly shortages and stockouts. By following some simple guidelines, you can ensure that your inventory is monitored and managed properly. So that you don’t run into any problems down the road.